The global offshore wind market is experiencing explosive growth. While Europe has been the leader in this industry, the Asia Pacific (APAC) region offers huge potential. Buoyed by ambitious clean energy policies and commitments to ensuring energy security, APAC is poised to be the frontrunner in the offshore wind industry over the coming decade. However, several issues need to be addressed. One of the key challenges is building the related transmission infrastructure, both offshore and onshore. Creation of a robust transmission system is critical to meeting the ambitious offshore wind targets in the region.

With this background, Global Transmission Report organised its second annual conference on Offshore Wind Transmission APAC virtually on April 12-13, 2022. The objective of the conference was to present the offshore wind opportunities in the Asia Pacific region, discuss strategies, and explore technologies and solutions for connecting upcoming projects to the grid. To this end, there were detailed discussions with policymakers, regulators, developers, transmission system operators, technology providers and industry experts to share their perspectives, learnings and issues.

The key takeaways from the conference are presented below.

Offshore wind – tapping the vast potential in APAC

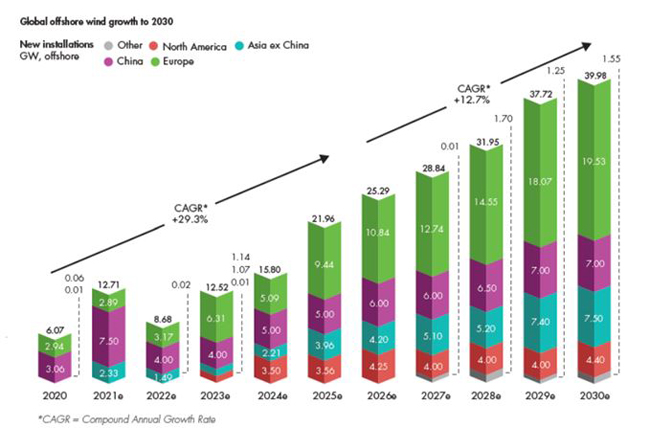

Chris Watkin, Global Marketing and Strategy Manager for HVDC, Hitachi Energy, presented the emerging opportunities and outlook for tapping the vast potential offshore wind (OSW) in APAC. He highlighted that by 2050, the global energy system will evolve and there will be significant electrification of final energy use at 44 per cent as compared to 20 per cent in 2020. Industries, transport and buildings are the key areas driving the demand for energy. Furthermore, power capacity will almost triple by 2050, with 80 per cent of the increase in power capacity expected to be comprised of renewables and storage. Furthermore, in the APAC region (particularly India, Vietnam, South Korea, Japan and Taiwan), 29 GW of OSW capacity will be added up to 2030, of which 8.8 GW will be added during 2021-25 and 19.9 GW in the 2026-30 period. Large potential is to be unlocked in Japan and South Korea from 2025, which will provide momentum for accelerated growth in these regions.

Figure 1: Global offshore wind growth till 2030

Source: Presentation by Chris Watkin, Global Marketing & Strategy Manager for HVDC, Hitachi Energy

He emphasised that to tap the offshore potential, the right turbine design is important. Going forward, he envisages an increase in the size of the wind turbine generators towards 15-20 MW. For storage, several floating tests are being conducted around the world, which will suit the deeper waters around some of the islands in the APAC region.

For grid connectivity, various HVDC links are supporting OSW around the world, particularly in Europe. One of them is the 300-km Caithness–Moray–Shetland link, which is the first regional DC grid in Europe. This is a multi-terminal system with five voltage source converter (VSC) stations. As per Chris, this technology is starting to mature, and can help tap OSW off various islands in the APAC region. Interconnection projects between Australia, Singapore and the islands in southeast Asia are under planning and development. Creating interconnections between regions and countries will be crucial for scaling up OSW in the region.

Challenges and opportunities for OSW in APAC

Narsingh Chaudhary, EVP and MD, Asia Pacific Black & Veatch, provided insights into the challenges and opportunities for OSW in APAC. He stated that OSW has the biggest growth potential of any renewable energy technology, but the policy environment needs to improve rapidly for offshore wind to reach international net zero targets. About 35 GW of OSW was installed in 2020. To close the OSW gap, there should be 270 GW of OSW installations globally by 2030 and 2,000 GW of OSW by 2050 to achieve zero net emissions by 2050 and maintain a 1.5°C pathway. To date, only the European Union (EU) has set a goal of 300 GW of OSW by 2050.

As per Narsingh, having an environmental policy in place is critical for OSW development. Some of the other key challenges perceived by developers include misaligned and delayed data presentations, capex cost overruns, logistical issues wherein equipment is not handled carefully, lack of careful planning of coastal operations, and transmission system integration, which is necessary to connect the available generation capacity to the grid. He shared the possible technology solutions and future options to address the challenges. These include regulatory support for environmental permitting and licensing; programme planning support for a good financial model; systematic feasibility study/financial model; proper material handling at ports including gathering, segregating and distributing the equipment; solid balance of plant (BOP) contractor; and efficient transmission and interconnection planning and studies.

Figure 2: Global offshore wind potential till 2050

Source: Presentation by Narsingh Chaudhary, EVP & MD, Asia Pacific Black & Veatch

Policies, plans and opportunities

Dr Chen Chung-Hsien, Director of Energy Technology Division, Bureau of Energy (BOE), Ministry of Economic Affairs (MOEA), Taiwan, discussed the status of OSW development in Taiwan, highlighting that the country has a three-phase programme underway to promote OSW development. Under the Phase 1 ‘Demonstration Incentive Program (DIP)’, the MOEA provides subsidies for both turbines and wind farms to encourage pioneers. Two projects—the 128 MW Formosa Demonstration Wind Farm and the 109.2 MW Taipower Demonstration Wind Farm—were commissioned under DIP in 2019 and 2021, respectively.

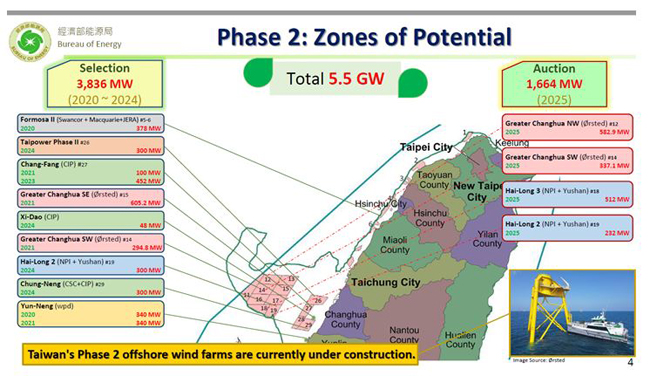

Under Phase 2, ‘Zones of Potential’ were introduced under which 3.8 GW of OSW capacity was allocated by selection and 1.7 GW of OSW capacity was allocated by way of auction in 2018. The wind capacity allocated under Phase 2 is under construction and 5.5 GW is expected to come into operation by 2025. Phase 3, ‘Zonal Development’, will run from 2026 through 2035 with an objective of developing 1.5 GW of OSW capacity every year amounting to a total of 15 GW during the 10-year period.

Regarding floating technology, the potential capacity in the feasible areas is about 12 GW, and MOEA plans to evaluate the feasibility of the demonstration project based on floating technology. The country plans to achieve an annual electricity production of 77.3 TWh from OSW, translating into an annual carbon reduction of 38.8 million tonnes. The foreign and domestic investment is estimated to exceed NTD3.2 trillion.

Figure 3: Offshore wind farms under construction under Phase 2 of Taiwan’s programme

Source: Presentation by Dr Chen Chung-Hsien, Director of Energy Technology Division, Bureau of Energy (BOE), Ministry of Economic Affairs (MOEA), Taiwan

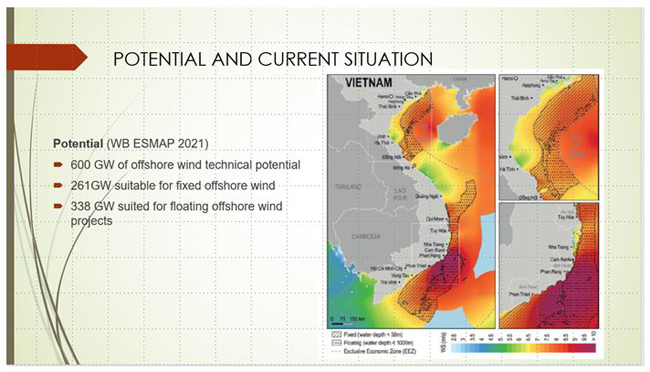

Mai Nguyen Phuong, Deputy Chief of the Office Electricity and Renewable Energy Authority (EREA), Ministry of Industry and Trade (MOIT), Vietnam, discussed the potential, plans and challenges of OSW development in the country. Vietnam has an estimated OSW potential of 600 GW (technical potential) of which about 261 GW is suitable for fixed OSW and the remaining for floating OSW technology. By the end of 2021, the country had an installed onshore wind capacity of 4,000 MW. As per the draft Power Development Plan VIII (PDP 8), Vietnam plans to develop 23,000 MW of wind power, of which 7,000 MW will be contributed by OSW power. Presently, over 70 GW has been registered for site investigation. OSW power is high on the Vietnam government’s agenda given the country’s target to reach net zero carbon emissions by 2050 as announced at the COP26 in November 2021. Also, OSW will be crucial in meeting the country’s high electricity demand, which is projected to grow by about 8 to 9 per cent annually during 2021-30, and by 4 to 5 per cent during 2031-45.

However, there are several legal, financial and infrastructural issues in OSW development. For instance, the Electricity Law and current regulations do not have specific regulations on OSW power development, the necessary technical infrastructure, and system operation regulations suitable for the market. There is also a lack of database and marine spatial maps for OSW. Further, the investment requirements are considerable. There are also manpower issues. The Vietnam government is looking at streamlining the policy by establishing a legal framework for OSW development.

Figure 4: Vietnam’s offshore wind potential

Source: Presentation by Mai Nguyen Phuong, Deputy Chief of the Office Electricity and Renewable Energy Authority (EREA), Ministry of Industry and Trade (MOIT), Vietnam

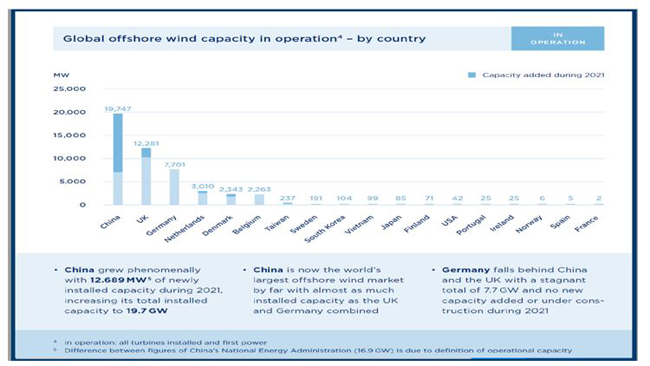

Joseph Deng, China Representative, World Forum Offshore, highlighted China’s achievements and plans in the OSW segment. He remarked that OSW power has grown phenomenally in China with 12,689 MW of newly installed capacity in 2021 increasing the country’s total installed capacity to 19.7 GW. China is now the world’s largest OSW market by far with almost as much installed capacity as the UK and Germany combined.

Currently, all major developers and utilities have onshore/offshore wind assets in China. Globally, 53 new OSW projects went into operation in 2021 with the maximum number, 45, in China. The high level of capacity addition in China in 2021 (~12.7 GW versus the global total of 15.7 GW) can be attributed to the expiration of the feed in tariff (FiT) regime in the country at the end of 2021. The average size of newly added OSW projects during 2021 was 296 MW compared to 347 MW in 2020 as many 200-300 MW projects were commissioned last year.

He further stated that going forward, China’s OSW power is expected to enter the era of parity. The sector is expected to grow rapidly with about 8 GW of capacity under construction. China’s OSW development will be driven by economic growth, falling costs and maturity of supply chain, as well as the country’s 2060 carbon neutrality goal.

Figure 5: Global offshore wind capacity in operation – by country

Source: Presentation by Joseph Deng, China Representative, World Forum Offshore

Ashish Khanna, President Renewables, Tata Power, spoke about the status and opportunities for OSW development in India. He said that India has huge potential for OSW power given its long coastline of over 7,600 km. The country has a mandate to reach 5 GW by 2022 and 30 GW by 2030, which offers significant opportunities to developers and stakeholders in this space. However, there are no OSW projects in India at present as the country is a latecomer in this segment and there is limited experience in terms of technology and infrastructure development. He remarked that it is necessary to derive learnings from the experience of global leaders in this space. Recently, Tata Power Renewable Energy Limited signed an MoU with the Germany-based RWE Group to explore the potential for development of offshore wind projects in India.

Further, he stated that there are several impediments to the development of OSW power in India. The first and foremost is the cost of OSW, which is several times that of onshore wind and solar projects. It also needs to be seen if OSW will be competing with solar and onshore wind or if the segment needs to developed on a standalone basis with support till the time it reaches a competitive level. There is a need to enable projects to come up on the rails quickly so that the learning curve of developers in this segment is steep.

In addition, he believes that the OSW segment needs to be supported not only in terms of tariffs (which will be high due to the high capex) but also through viability gap funding or other policy measures. Further, for long-term sustainable development of the segment, infrastructure needs to be planned well and the Indian government needs to give a project pipeline to investors, contractors and other stakeholders.

Developers’ plans and perspective

Bernard Casey, Chief Operating Officer, Mainstream Renewable Power, discussed current OSW development in Vietnam and Japan as well as potential opportunities in the Philippines. The OSW market in Vietnam is still at a nascent stage with new challenges and opportunities.

He also discussed the grid challenges for OSW. The most difficult challenges for offshore transmission appear to be onshore grid capacity and optimal locations for projects, which are often far from load centres. Bernard shared that to address the issue of the distance between the best renewable energy resource and load centres, some utilities such as South Africa’s Eskom are implementing, upgrading and planning major grid projects, including 765 kV transmission lines and substations, over the next 10 to 15 years. Further, some US companies have adopted smart wires modular technology, which balances flows on the grid to maximise transfer capacity, to bring more renewables and reduce costs. Several national grids across different continents are deploying this technique to increase local capacity.

As per Bernard, an emerging trend is superconductors, driven mainly by the limited availability of copper for future enhancement and development of the electricity network. Superconductors are more efficient for bulk power transfer and are ideal for underground installations. They can be useful in avoiding urban congestion and in achieving large-scale grid reinforcement.

Pelayo Rodríguez Alonso, Senior Business Development Manager, Ocean Winds, elaborated on the potential of floating OSW as the future technology and its scope in the Asian market. He highlighted that this technology will be relevant as many countries do not have shallow waters off their shores. He stated that Ocean Winds has made significant developments in South Korea, where it has a bankable floating offshore farm totalling 1,300 MW. Another project under development in the region is the 1,245 MW Hanbando OSW farm. In Asia, the company is looking to make inroads in India, Vietnam, Philippines and Indonesia, and is focused on developing and strengthening the pipeline in Asia. Globally, the company has 1.5 GW of OSW under construction and operation while another 9.8 GW is under development across seven geographies. It is involved in several active offshore projects, including three in the UK and Scotland, and in Portugal, France and the Atlantic. It is also present in the Netherlands, Norway, Spain, Italy and Greece, where it has received a positive response.

Elena Farnè, Technical Director, Equinor, estimates that by 2030, the company’s share in OSW installed capacity will increase to 12-16 GW, for which substantial investments will be made during 2021-26. In Asia, Japan and Korea will be big contributors to achieving Equinor’s OSW targets. It plans to build a mixed pipeline of projects in South Korea and Japan, including bottom fixed and floating, to help deliver the two countries’ compensation targets, which are 10 GW by 2030 for Japan and 12 GW for Korea. Japan’s wind resources and green infrastructure are mainly in areas with high wind speeds such as southern Okinawa and nearby islands while transmission line connections are mainly in and around Tokyo and Greater Tokyo. Also, the split of the market in Japan between 60Hz and 50 Hz makes it difficult to balance the system. Similarly, in South Korea the demand centres are in and around the Seoul and greater Seoul areas. Further, solar energy is also a good contributor to delivering power to the grid in South Korea.

Floating OSW opportunity and technology in APAC

Marcus Dowling, Engineering Lead, Flotation Energy, presented the floating OSW opportunity in APAC. He highlighted that offshore floating wind removes key constraints and provides economic advantages, which include access to more ocean site locations; creates local industry opportunities; leads to higher yields and availability; reduces seabed impacts; is less intrusive (fisheries, shipping, visual); provides for onshore assembly and commissioning; and leverages existing Taiwanese industry expertise.

He mentioned that in 2022, there will be 127.9 MW of floating OSW installed capacity, which is estimated to increase to 70 GW by 2040. Key markets include UK, Ireland, Norway, France, Portugal, Spain, Taiwan, Japan, South Korea, China, California, Maine and Hawaii.

Flotation Energy developed the 50 MW Kincardine—the world’s largest floating OSW farm. Some of its floating OSW projects in APAC include the 1.2 GW Chu Tin (Hsinchu) floating OSW farm in Taiwan; and the 1 GW Toki (Niigata), 450 MW Kishuu (Wakayama) and 520 MW Sakura (Chiba) floating OSW farms in Japan.

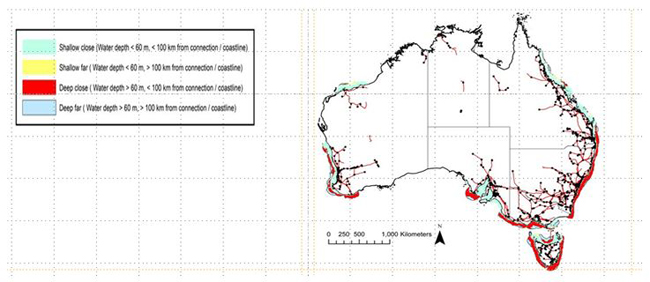

He also shared an update on Australia’s OSW policy scenario. Australian legislation for OSW will become effective in June 2022. Further, the first declaration of suitable areas for offshore renewable energy infrastructure is targeted off the south coast of Victoria State, near Gippsland. Also, draft offshore regulations were out for consultation until the end of April, and will be managed by the National Offshore Petroleum Safety and Environmental Management Authority (NOPSEMA) and environmental referrals are still required under the Environmental Protection and Biodiversity Conservation Act 1999. According to the technical national OSW assessment performed by Blue Economy Cooperative Research Centre, Australia has a constrained OSW potential (both fixed and floating) of 2,200 GW.

Figure 6: Australia’s fixed bottom and floating OSW

Source: Presentation by Marcus Dowling, Engineering Lead, Flotation Energy

Ao Zhang, Business Development Manager, Principal Power, discussed the company’s Windfloat floating technology and highlighted some of the unique design features. Currently, the company is focusing on industrialisation and utility scale projects such as the 1.2 GW project in South Korea and a 400 MW project in Hawaii. The company also has a shallow water solution (water depth of 40-60 metres) for projects in the APAC region. It can also design specific models for the typhoon-prone regions of Japan, Korea, China and Taiwan.

The company has conducted three pre-commercial projects—the Windfloat Atlantic (WFA) project in Portugal, the Kincardine project in Scotland and the Les Eoliennes Flottantes Du Golfe Du Lion (EFGL) project in France. WFA and Kincardine have been commissioned and are operational while the 30 MW EFGL project is in the fabrication phase and will be operational in 2023.

For the APAC region, factors such as extreme weather conditions, hurricanes, tsunamis etc. must be considered as they have an impact on the weight of the platform. As per Zhang, capacity is the key driver to reduce the cost of floating wind and adequate transmission infrastructure is required to take projects to commercial scale.

Optimal transmission technology

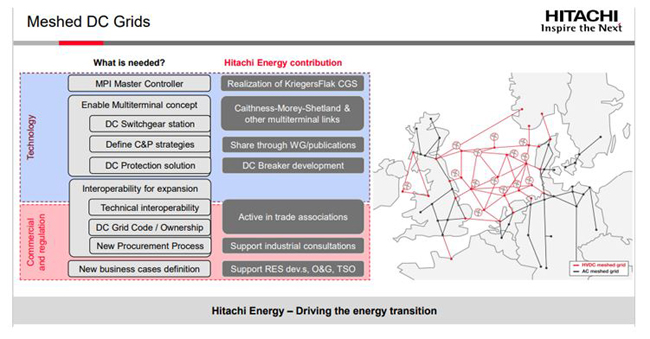

Peter Sandeberg, Global Product Manager, Offshore Wind Connections, Hitachi Energy, presented the optimal transmission technologies for OSW in APAC. As per Peter, the exponential growth of the OSW sector has been driven by technical developments and grid transformation needs, and HVDC will play a major role in the future. To advance OSW, there is an urgent need for mainland grid reinforcements as well as a coordinated offshore grid approach. He highlighted the key trends in OSW and offshore grid technologies including the increase in the size of wind turbine generators (WTGs) towards 15-20 MW; an increase in collection grid voltage from 66 kV to 110/132 kV; the development of 2 GW, 525 kV bipolar solutions; hybrid solutions (interconnection + offshore wind connections), offshore power hubs/energy islands, meshed DC grid mainland grid reinforcement; and the development of power2X (hydrogen) technology, energy storage and floating wind farms. He shared that Hitachi Energy has been an integral part of and contributed to the development of meshed DC grids such as Kriegers Flak CGS (completed) and the Caithness–Moray–Shetland link and other multi-terminal links.

Figure 7: Progress of meshed DC grids

Source: Presentation by Peter Sandeberg, Global Product Manager, Offshore Wind Connections, Hitachi Energy

Planning and designing grid integration

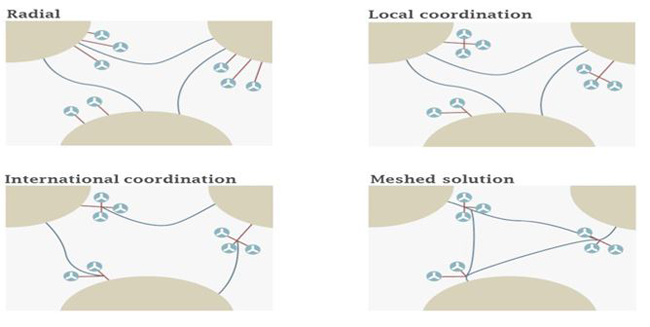

Joo Duk, Director, Elia Grid International (EGI) Pte Limited, discussed the key technical design choices for offshore grid development including radial versus meshed, local versus cross-border, and hubs as platforms or artificial islands. He also spoke about how grid integration design can minimise infrastructure cost, maximise access of renewable energy and ensure high reliability standards while complying with grid codes and minimising the environmental impact of grid infrastructure. Joo also made a case for hybrid interconnectors and mentioned some of the key measures required to promote them including reduction in complexities and risks by structuring projects according to their individual components, securing a conducive investment climate for the speedy delivery of projects, ensuring a fair share of benefits for countries with different interests, and the development of offshore market bidding zones to maximise benefits.

Figure 8: Four archetypes of offshore grid infrastructures

Source: Presentation by Joo Duk, Director, Elia Grid International (EGI) Pte Limited

Riccardo Felici, Vietnam Country Manager and Subsea Cable Installation Expert, OWC Ltd, discussed various challenges involved in exporting power from offshore production points to consumption/demand hubs. He spoke in detail about the different types of connections between the wind turbine generators (WTG) and the substation (star, radial and ring) and their pros and cons.

Riccardo stressed on producing initial concept electrical designs to explore different options along with cost benefit analysis and then refining them to have options at the conceptual stage. He also touched upon route options and recommended considering all available survey information and/or desk-based data sets so as to determine the optimal cable route. He also called for cooperation among key stakeholders to ensure all routing constraints are considered.

O&M and protection of subsea cables

Alicia Stammers, Associate, and Robert Keast, Manager, Carbon Trust, shared the company’s recent work on OSW, especially under its Offshore Renewables Joint Industry Programme (ORJIP), Floating Wind Joint Industry Programme (FLWJIP), the Integrator and the Offshore Wind Accelerator (OWA) programme. These programmes take an industry-led approach to research and development. For instance, the key objectives of OWA include lowering the cost of OSW, overcoming market barriers, promoting innovative and best practices, and triggering the development of new industry standards. Research and work under OWA are focused on areas such as subsea cabling; logistics, operations and maintenance; electrical systems and transmission; bottom-fixed foundation aspect and yield and performance of turbines. Under the OWA, Carbon Trust recently completed the High Voltage Array Systems project, which was aimed at developing a future-fit array system for OSW.

The upgrade of array cable voltage enables efficient power collection and unlocks cost savings to reduce evelized cost of energy (LCOE). He highlighted that the next array systems would operate at 132 kV, major investments in 132 kV wind farms would take place by the mid-2020s, followed by energisation of wind farms by the late-2020s, increasing availability of 132 kV turbines, testing reliability and standards of 132 kV wet cables, boosting installation methods of 132 kV cabling and emphasising on cost uncertainty for 132 kV cables, switchgear and turbines. The wind turbine capacity was 3.6 MW in 2008, which increased to 12 MW in 2019. The company has set a target of increasing this to over 15 MW by 2025 for a future-fit array system.

Morten Huseby, Chief Executive Officer, Wirescan AS, focused on next generation asset health assessment and monitoring of cables. He highlighted the reasons for poor and costly cable health, which include poor manufacturing of cables; poor spooling and transportation; installation issues like terminations, splicing and joints of cables; damages by cable breakdown; unpredictable downtime, resource management and capex and opex; and imminence of cable failures. There are various cable health assessment technologies, particularly line resonance analysis (LIRA). This caters to both offline and online technology solutions. It is a non-destructive and legal technology indicating global and local values of cable health.

He shared that Wirescan aims to help its clients fix typical cable failiures and opt for predictive prevention to use data. Cloud analysis and the reporting process revolve around three steps, namely, cable grid data acquisition, maintenance plan execution and automatic and expert decisions. The company’s digital solution is capable of easy and semi-automated LIRA data acquisition, aggregation and analysis of relevant cable health data, cable health data centralisation and digitisation, and cloud-based analysis of cable health data.

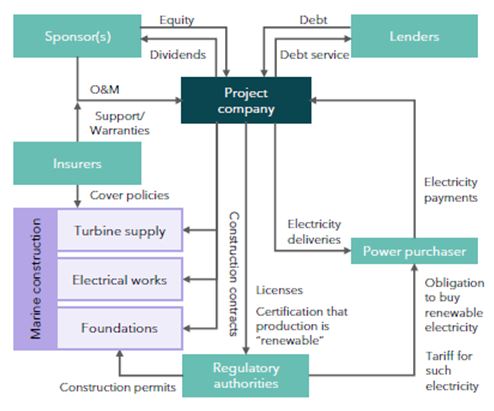

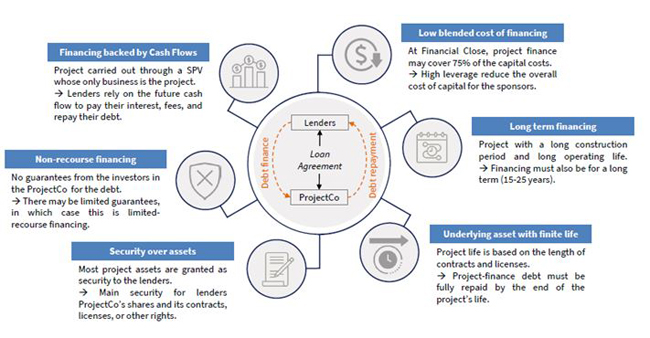

Financing offshore wind

Matthew Taylor, Managing Director, Green Giraffe, highlighted that offshore wind technology requires a large amount of capital to be invested in a small number of assets. Because of the large sums involved, he called out for due diligence while arranging these funds. He further stated that over the last few years, OSW has been successful because of the levelised cost of energy (LOCE) coming down substantially. However, he pointed out that because the LOCE has come down at a very fast pace, it has raised problems for supply chain pricing, which is now going up rather than continuing to go down.

Matthew also discussed that OSW transactions are always heavily contracted. Major contracts include permits, licences, authorisations, etc. Parties with a stake in the financing and a say on the overall project structure may include sponsors/investors, lenders, contractors, insurers etc.

He further observed that in APAC specifically, a large number of aggressive players have emerged in the offshore wind industry. He concluded by saying that there is tremendous opportunity for offshore wind but there is also a need for realism in terms of how to develop these assets.

Figure 9: Offshore wind project financing

Source: Presentation by Matthew Taylor, Managing Director, Green Giraffe

Quentin Le Noac’h, Investment Director, Amsterdam Capital Partners, emphasised the huge scope for OSW in the APAC region with multiple GW of capacity being installed over the next decade. He also touched upon various sources of financing these huge projects, i.e., corporate financing, which can be further broken down into international bonds and local bonds, and project financing, which can further be categorized into syndicated loans and green bonds.

Quentin also discussed some of the key challenges in the APAC market, which include early stage and limited capacity of the Asian supply chain for most project components; different climate and soil conditions as compared to Europe requiring adaption by industry; higher subsidies required to make floating wind viable with governments’ views on the same; and revenues typically being in the local currency while funding for large projects typically has international currency components. He concluded by saying that the experience in Europe could be useful while developing the OSW market in the APAC region.

Figure 10: Key features of project finance

Source: Presentation by Quentin Le Noac’h, Investment Director, Amsterdam Capital Partners

James Theobalds, Associate Director, Transactions, Arup, spoke about the differences between the APAC region and Europe in terms of delivery frameworks, requirements around supply chain and level of coordination among APAC countries as compared to Europe. Nonetheless, he emphasised the solid offshore project pipeline in APAC over the next decade, pointing to the immense opportunities for the offshore industry and investors.

James stressed that the role of the regional governments would be critical in the development of the offshore markets and that the governments should provide long-term policy stability and project pipeline visibility to help build industry confidence and the ability to invest. He also discussed how investors need transparent processes to enable key project delivery milestones.

Outlook for offshore wind in APAC

Kaori Tachibana, Associate Director, Gas, Power & Climate Solutions, S&P Global, shared that OSW is playing a key role in driving the global energy transition. The global OSW capacity has increased from 3 MW in 2010 to 60 GW in 2021. In Asia, OSW capacity is expected to grow to over 300 GW by 2030 from 5 GW in 2018. Particularly, by 2030, OSW capacity is expected to grow to 7 GW in the Republic of Korea, 13 GW in Japan, 6 GW in Vietnam, 3.5 GW in India and 9 GW in Taiwan.

She also discussed the key trends in the OSW market in APAC. OSW development has been steadily expanding since 2020 and supply in all markets has increased as a result of the nearly tenfold increase in the installed capacity as compared to 2020. The permitting process of the announced capacities is complicated, which poses a threat to projects and their development. The framework for OSW development allows a bottom-up approach for a comprehensive selection process, but a clear contractor selection process and high subsidy level especially for floating OSW would yield better results. Between 2026 and 2035, there seem to be increasingly restricted areas for offshore development and it will be challenging for countries to achieve their 2050 targets. The market development potential has increased based on the current power market regulation, status, availability of policies and subsidies to support the development. Finally, renewable generation facilities are more cost competitive than traditional power generating technologies.

Figure 11: Offshore wind capacity additions are starting to accelerate in APAC

Source: Presentation by Kaori Tachibana, Associate Director, Gas, Power & Climate Solutions, S&P Global

(NTD1=USD0.034)